Home

Posts

About Us

Home

Posts

About Us

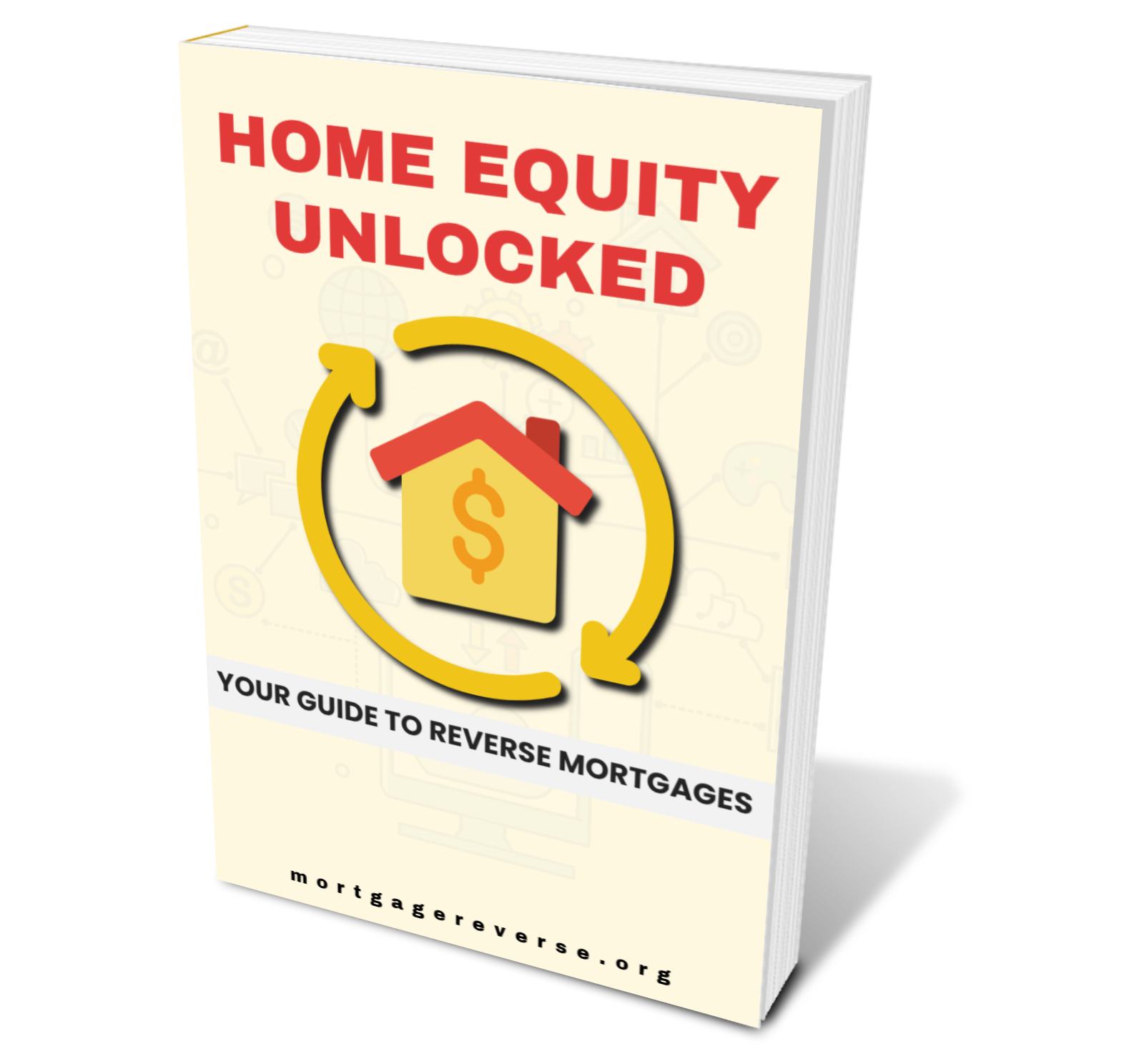

Home Equity Unlocked:

Your Guide to Reverse Mortgages

Download Our Free Guide and Start

Navigating Reverse Mortgages with Confidence

Enter your Name and Email Below For Instant Access

We Respect Your Privacy

Free Reports

Reverse Mortgage Underwriting: Balancing Risk, Regulation, and Financial Freedom

Reverse Mortgage Tax Implications: A Guide to Managing Taxes, Benefits, and Inheritance

Reverse Mortgage Tax Considerations: A Guide to Financial Planning and Benefits Management

Reverse Mortgage Repayment Plans: Options, Responsibilities, and Strategies for Success

Reverse Mortgage Refinancing: Costs, Benefits, and Alternatives for Financial Flexibility